"5 Signs of a Competitive Advantages" : Hints Hidden in the Financial Statements

Discover how to identify a company’s economic moat through financial statements. This article reveals the hidden hints of competitive advantage — from favorable terms of trade and consistent growth to high ROA, strong internal accruals, expanding book value, and a healthy dividend payout. Learn how these subtle financial signs indicate enduring business strength and long-term wealth creation.

FINANCE

Arya H Parekh

10/10/202511 min read

Have you ever wondered why some companies seem to grow effortlessly year after year — while others fade away despite early success? The answer often lies in something invisible yet immensely powerful: their economic moat.

As we discussed in our previous blog on the types of economic moats, we discussed that, identifying businesses with durable competitive advantages is the key to finding those rare compounding machines — the ones that protect profits, sustain growth, and stay ahead of the competition for decades.

But here’s the tricky part — how do you actually spot them? The truth is, moats don’t come with a label. They’re hidden somewhere deep within the company — often so well that even seasoned investors struggle to find them. Yet, if you look closely, these clues quietly reveal themselves in the company’s numbers — in patterns that hint at something special beneath the surface.

That’s right — the financial statements often tell the real story. Behind all the noise of stock prices and quarterly results lie subtle hints of enduring strength — things like consistent returns, self-funded growth, and expanding book value.

In today’s post, we’ll uncover those financial clues — the kind successful investors rely on to separate truly durable businesses from those merely enjoying a good season. By the end, you’ll see how to read between the lines of a company’s financials to spot the kind of moat that not only protects profits — but compounds wealth for years to come.

1. Favorable Terms of Trade (Customer Advances)

Favorable terms of trade play a key role in how efficiently a company manages its working capital. When a business has the power to decide when and how it gets paid, it reflects strong customer trust, brand strength, and bargaining power.

As investors, we all want to own companies that operate in a seller’s market — those that can sell on their own terms.

In today’s world, most businesses are trapped in a buyer’s market, where they have to constantly lure customers through discounts, coupons, and endless sale offers just to move their products. The result?

A large portion of their money gets tied up in high working capital needs.

Working capital represents the short-term funds a company needs to run its operations smoothly. It can be calculated using the basic formula:

Working Capital = Trade Receivables + Inventory – Trade Payables

Most companies operate with positive working capital, meaning they first spend on raw materials and inventory before receiving cash from customers.

But in a business world where everyone is busy chasing customers, it’s rare — and remarkable — to find a company that has customers lining up and are ready to pay in advance.

This can even sometimes leads in negative working capital, where a company collects money before paying its suppliers — typically through customer advances.

That’s can be the sign of a business with real strength.

When a company can dictate the terms of trade, it doesn’t just enjoy higher margins — it often requires no working capital at all, because customers are funding its operations.

Examples: Eicher Motors and Force Motors

Take Eicher Motors, the maker of Royal Enfield. Many of its models come with a waiting period of two to three months, yet customers happily pay booking amounts upfront.

That’s not a marketing trick — that’s brand power and customer loyalty. It shows the company’s ability to set its own terms, even in a market overflowing with options.

A similar trend is visible in Force Motors, where customer advances have been rising rapidly in recent years. This reflects growing demand visibility and the company’s increasing control over its trade terms — both key indicators of long-term business strength.

“When customers are ready to pay before they receive the product, and suppliers are ready to wait for payment — you’re looking at a company that’s truly in control.”

The Cash Flow Advantage

There’s another sign of a moat that’s closely connected to this — cash flow superiority.

A company shows real financial strength when it can consistently convert more cash flow from operations (CFO) than its reported profits.

Why does this happen?

Because customer advances and supplier credit improve operational cash generation — even if the accounting profits stay the same.

Such companies convert earnings into cash efficiently, which is one of the clearest signs of business quality. Strong cash conversion means the company isn’t just generating paper profits — it’s generating real money that can be reinvested for growth, used to reduce debt, or returned to shareholders.

This combination of brand-driven demand, bargaining power, and superior cash flow conversion is what separates great businesses from good ones.

Profitability + Favorable Terms of Trade = Multi-bagger Potential

2. Consistency And Predictability of Earnings

Another key sign that reveals the true durability of a business is the consistency and predictability of its profits. When a company has been generating profits steadily over the years, it not only proves its business strength and Brand power but also gives investors the confidence and predictability of cash flows that it can continue doing so over the next 5 to 10 years. In determining predictability one of the first things an investor should look at to see how old the company is.

“I look for business in which I think I can predict what they’re going to look like in 10 to 15 year time. Take Wiggly chewing gum. I don’t think the Internet is going to change how the people chew gum” – Warren Buffett

If a company’s earning history is erratic, it often indicates a commodity-type business, where the product has no brand identification and competes in the marketplace solely on the basis of price. In such industries, profits depend more on external market conditions and your ability to understand market cycles correctly.

Where else on the other side a company that has been operating in the same industry for more than 10 to 20 years, selling the same brand, product, or service, and maintaining a consistent upward earnings trend likely has a durable competitive advantage working in its favor. Such companies also benefit from experienced management, which has witnessed multiple business cycles and already learned to navigate both upturns and downturns effectively.

As market loves the factor of predictability into the business giving it a higher PE multiple for in the market. Even Warren has emphasized that companies lacking long-term consistency in earnings often make poor long-term investments, as they lack the stability and competitive moat required to create shareholder wealth.

A great example of this is CCL Products (India) Ltd., one of the world’s largest high-value-added coffee processors and instant coffee manufacturers. The company follows a cost-plus model, which allows it to pass on raw material price fluctuations to its clients. Despite operating in a commodity-driven industry, where coffee prices have at times surged nearly fivefold, CCL has consistently maintained sustainable EBITDA per tonne.

What’s even more remarkable is that CCL has grown its sales and profits at a steady 18–20% CAGR over the past decade. This ability to deliver consistent compounding, reflects a durable competitive advantage and disciplined management execution — hallmarks of long-term wealth creators.

“Consistent and predictable profits are the clearest signs of a company built to last."

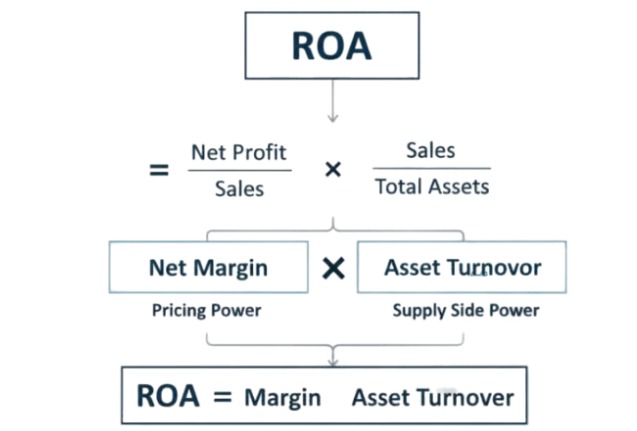

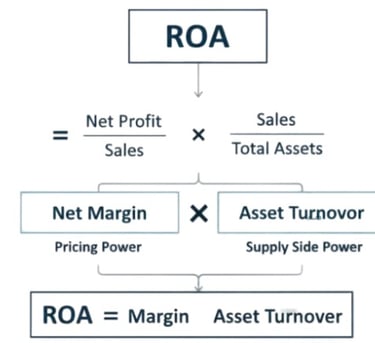

3. Return on Asset (ROA) > 10%

Another key sign of a durable competitive advantage is a consistently high Return on Assets (ROA), typically above 10%.

ROA measures how efficiently a company uses its total assets to generate profits. In simple terms, it tells investors how much profit a company earns for every ₹100 invested in assets. A higher ROA indicates that the business is effectively converting its resources — machinery, inventory, and capital — into earnings.

But you might be wondering — how can such a simple ratio tell us about the durability of a business?

One of the best ways to understand this is through the DuPont Analysis, which breaks ROA into two key components:

i). Pricing Power – High Profit Margins

Companies with strong pricing power can maintain high margins because customers are willing to pay premium prices for their products.

This often comes from brand strength, product differentiation, or intellectual property that limits competition.

A great example is Divi’s Laboratories. The company operates in niche segments of active pharmaceutical ingredients (APIs) where quality, reliability, and regulatory compliance are critical. Because of its technical expertise and strong client relationships, Divi’s enjoys industry-leading margins. Customers pay a premium, not just for the product but for the trust and assurance that comes with it.

As investors, it’s important to look beyond the numbers and ask: What allows this company to maintain high margins?

It could be brand reputation, high switching costs, proprietary technology, or regulatory advantages (Already covered in our previous blog- Types of Economic Moats )— all of which signal the presence of a moat based on pricing power.

ii). Supply-Side Power – High Asset Turnover

On the other hand, companies with high asset turnover generate more revenue per rupee of assets. This efficiency usually comes from scale, cost leadership, or superior execution on the supply side. Lets take APL Apollo Tubes, for instance. It has built one of the most efficient manufacturing and distribution setups in the steel tubes industry. Its ability to rapidly turn assets into sales results in exceptional asset turnover ratios.

This efficiency often stems from continuous capacity expansion, which can take three main forms:

Greenfield Expansion – Setting up new facilities from scratch.

While it increases long-term capacity, it usually requires heavy capital investment, resulting in lower asset turns in the initial years.

Hence, it’s least accretive in the short term.

Brownfield Expansion – Expanding existing plants to increase production.

This approach is more accretive than Greenfield since it leverages existing infrastructure and management experience but still demands moderate capital.

Debottlenecking – Improving existing processes or optimizing machinery to enhance capacity without major investments.

This is the most accretive form of expansion, as it creates additional output with minimal capital expenditure, leading to higher asset turnover and better ROA.

Thus, companies that continuously improve efficiency through debottlenecking or smart brownfield expansions often sustain high ROA for long periods — a hallmark of a moat built on supply-side strength. So, when a company maintains ROA above 10% consistently over several years, ask yourself whether it comes from pricing power or supply side power !

Which Is Better — High Margins or High Asset Turnover?

While both are valuable, it’s generally better for a company to have high asset turnover rather than just high margins.

High margins often attract competition. When an industry shows abnormally high profitability, it tempts new entrants, leading to price wars and eventual margin erosion. In contrast, high asset turnover is much harder to replicate. It reflects a company’s scale advantage, cost leadership, and process excellence — all of which are built gradually and cannot be easily copied.

4. Growth Through Internal Accruals ( No equity dilution )

Businesses that fund their expansion through retained earnings, rather than relying on frequent equity dilution or heavy debt, demonstrate genuine financial strength.

Growth driven by internal accruals reflects self-sustainability and reliable cash generation because of which company even faces any difficult period it still has the ability to sustain even in the difficult period as compare to the company which is highly leveraged. This are the hallmarks of high-quality companies with durable business models.

As veteran investor Chandrakant Sampat once said:

“I will buy only those businesses which even a fool can understand, have little debt, have free cash flows, or do not have much capital expenditure.”

What he meant was simple — the best businesses are those that can grow using their own money, by converting accounting profits into real cash and reinvesting it back into the business to fuel further growth. These are often asset-light models, where capital efficiency and cash generation go hand in hand.

Let’s take a small company named ECOs Mobility. It is one of the most reputed car rental service providers in India, offering both chauffeured car services and employee transportation solutions. What’s most fascinating about this company is its asset-light business model — over 90% of its fleet is vendor-owned, which allows the company to scale rapidly without relying heavily on external funding or equity dilution.

By following this model, ECOs Mobility manages to grow sustainably while generating strong free cash flows, a clear sign of financial discipline and long-term compounding potential.

5. Growing Book Value Over Time

Its one of the a simple yet powerful indicator of moats, famously used by Warren Buffett, is the consistent growth in its book value over time. Buffett has long used the growth in Berkshire Hathaway’s book value as a yardstick for measuring its long-term economic performance.

Book value, as we know, represents a company’s net worth — total assets minus total liabilities. When book value compounds steadily over long periods, it shows that the company is retaining its earnings and reinvesting them profitably, often signaling the presence of a sustainable competitive moat.

Buffett once explained:

“We give Berkshire’s book value figures because they serve as a rough, albeit significantly understated, tracking measure for Berkshire’s intrinsic value. In other words, the percentage change in book value in any given year is likely to be reasonably close to that year’s change in intrinsic value.”

While book value is not the same as intrinsic value, but it can serve as a loose method for measuring company's economic performance and helps identify companies with durable competitive advantage. Let's see how -

Intrinsic value is theoretically the present value of all future cash flows — a concept that’s precise in theory but almost impossible to estimate accurately in practice.

However, over time, the growth rate of book value tends to move in line with the change in intrinsic value, especially for businesses that retain most of their earnings.Growth in book value essentially reflects the return a company earns on its equity base — in other words, its Return on Equity (ROE).

A company that grows book value consistently while maintaining high ROE likely enjoys a durable edge — through brand strength, cost efficiency, distribution power, or entry barriers.

Once we have identified its presence, then we can dig deeper into the company economic history help us determine whether a durable competitive advantage is truly present.

In short, tracking book value growth acts as a quick acid test. It helps investors identify companies that have demonstrated the power of compounding — those rare businesses that quietly build wealth year after year through disciplined capital allocation and competitive strength.

(Bonus) 6. Consistent Dividend Payouts

Another bonus trait we noticed while studying the portfolios of legendary investors like Raamdeo Agarwal, Ramesh Damani, Govind Parikh, and Hiren Ved is that the companies they back often show a consistent dividend payout ratio.

This isn’t just about rewarding shareholders — it’s a quiet signal of predictability, financial stability, and enduring strength. A company that can share profits year after year without compromising growth is one that likely enjoys steady cash flows and a durable competitive edge.

In fact, one of the most telling signs you can find in a company’s financial statements to assess the quality and durability of its business is the consistency of its dividend payouts. It reflects discipline, resilience, and the kind of moat that keeps compounding over time.

Before diving deeper, let’s understand what a dividend payout actually means. A dividend payout is the portion of net profits distributed by a company to its shareholders as a reward for their investment.

It is true that regular and stable dividend payouts are often seen as a sign that the company consistently generates profits and values shareholder returns. However, a deeper look reveals that dividend consistency reflects two critical dimensions — the character of the business and the quality of management.

1. The Character of the Business

A company can pay dividends only when its profits turn into real cash flows. If it has maintained payouts of 25-30% for years, it shows a strong ability to convert profits into cash — a clear sign of a stable and sustainable business model.

2. The Quality of Management

Consistent dividends also reflect the intent and wisdom of management. It shows their commitment to sharing profits with shareholders instead of keeping idle cash, highlighting transparency, accountability, and efficient capital use.

To understand this concept better, you can refer to our previous blogs on Bharat Shah , where we’ve discussed how dividend policies reflect a company’s financial health and management philosophy.

“So, the next time you study a company’s financials, look beyond the numbers — focus on the signs of a moat reflected in favorable terms of trade, consistent growth, high ROA > 10% ,No equity dilution, growing book value, and a healthy dividend payout. These are the quiet signals of enduring strength.

Happy Investing!”

Investing & Finance

Develop the Right mindset of investing in the indian stock market from the masters.

Join our Master Investor Community and develop the Right mindset of investing

Subscribe

contact - arya@masterinvesting.in

© 2025. All rights reserved.